According to the new market research report Contract Manufacturing in Medical Device Market is estimated to reach USD 113. The key factors driving the growth of the Contract Manufacturing in Medical Device Market include the overall growth of the medical devices market, mainly due to rising disease prevalence, life expectancy, and the geriatric population. id=170622851However, market growth is impeded by the growing consolidation in the medical devices market. Class II medical devices segment accounted for the largest share of the Contract Manufacturing in Medical Device Market in 2020. In 2020, the device development and manufacturing services segment accounted for the largest share of the marketBased on service, the medical device contract manufacturing market is segmented into device development and manufacturing services, quality management services, packaging and assembly services and other services.

0

Based on product, the market is segmented into thoracic fusion and lumbar fusion devices, cervical fusion devices, spine biologics, non-fusion devices, vertebral compression fracture treatment devices, spinal decompression devices, and spine bone stimulators. Browse in-depth TOC on "Spinal Implants Market"314 – Tables32 – Figures269 – PagesThe spinal fusion and fixation technologies segment accounted for the largest share of the Spinal Implants Devices Market in 2019. On the basis of technology, the Spinal Surgery Devices Market is segmented into spinal fusion and fixation, vertebral compression fracture treatment, motion preservation/non-fusion, and spinal decompression technologies. North America dominates the Spinal Implants Market. id=712The major players operating in the Spinal Implants Market are Medtronic (Ireland), DePuy Synthes (US), NuVasive, Inc.

0

Browse and in-depth TOC on "Minimally Invasive Surgical Instruments Market"237 - Tables43 - Figures274- PagesDownload PDF Brochure: https://www. Emerging economies such as China, Japan, and India are providing lucrative opportunities for the players operating in the MIS Instruments Market. The handheld instruments segment accounted for the largest share of the minimally invasive surgical instruments market, by product segment, in 2020Based on product, the market is segmented into handheld instruments, inflation devices, surgical scopes, cutting instruments, guiding devices, electrosurgical & electrocautery instruments, and other instruments. In 2020, the hospitals and specialty clinics segment accounted for the largest share of the minimally invasive surgical instruments market. North America is the largest regional market for minimally invasive surgical instruments marketThe global MIS Instruments Market is segmented into five major regions—north America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa.

0

Browse in-depth TOC on "AEDs Market"132 – Tables30 – Figures158 – PagesThe ICDs segment accounted for the largest share of the market in 2019On the basis of type, the market is segmented into implantable cardioverter defibrillators (ICDs) and external defibrillators. The ICDs market is further segmented into transvenous implantable cardioverter defibrillators (T-ICDs) and subcutaneous implantable cardioverter defibrillators (S-ICDs). The External Defibrillators Market is further segmented into manual and semi-automated external defibrillators, fully automated external defibrillators, and wearable cardioverter defibrillators (WCDs). The ICDs segment accounted for the largest share of the market in 2019. In 2019, North America accounted for the largest share of the Defibrillators MarketIn 2019, North America accounted for the largest share of the market.

0

According to the new market research report The laboratory information systems market is projected to reach USD 2. id=232312738By delivery mode, cloud-based LIS to register the highest CAGR during the forecast periodBased on delivery mode, the LIS market is segmented into on-premise and cloud-based LIS. The cloud-based LIS segment is expected to register the highest CAGR during the forecast period. By product, the standalone LIS segment accounted for the largest market share in 2018Based on product, the LIS market is segmented into standalone LIS and integrated LIS. North America dominated the LIS market in 2018; this trend to continue during the forecast periodGeographically, the LIS market is divided into North America, Europe, Asia Pacific, and the Rest of the World (RoW).

0

According to the new market research report "Medical Radiation Detection, Monitoring and Safety Market by Detector (Gas-Filled, Scintillators, Solid-State), Product (Personal Dosimeters, Passive Dosimeters) Safety (Full-Body Protection) & End User (Hospitals, Non-Hospitals) - Global Forecast to 2027", published by MarketsandMarkets™, the global Medical Radiation Detection, Monitoring, and Safety Market is projected to reach USD 1. Browse in-depth TOC on "Medical Radiation Detection, Monitoring, and Safety Market"401 – Tables42 – Figures336 – PagesDownload PDF Brochure: https://www. Emerging economies such as China, Japan, and India are providing lucrative opportunities for the players operating in the medical radiation detection & safety market. id=1200 Full-body protection segment accounted for the largest share in the market, by medical radiation safety productsThe medical radiation detection, monitoring, & safety market is segmented into full-body protection products, face protection products, hand safety products, and other medical radiation safety products. North America is the largest regional market for medical radiation detection, monitoring, & safety marketThe global medical radiation detection market has been segmented into four major regions—North America, Europe, the Asia Pacific, and Rest of the World.

0

This report aims to provide insights into the global cancer immunotherapy market. Browse 43 market data Tables and 69 Figures spread through 145 Pages and in-depth TOC on "Cancer Immunotherapy Market"Download PDF Brochure: https://www. id=197577894In this report, the global Cancer Immunotherapy Market has been segmented based on type, application, end user, and region. On the basis of end users, the global Cancer Immunotherapy Market is segmented into hospitals and clinics & others. On the basis of applications, the global Cancer Immunotherapy Market is segmented into lung cancer, breast cancer, colorectal cancer, melanoma, prostate cancer, head & neck cancer, and others.

0

Browse 143 Market Data Tables and 33 Figures spread through 187 Pages and in-depth TOC on "Weight Loss Obesity Management Market"Download PDF Brochure: http://www. id=1152Beverages segment to dominate the market in 2017Based on diet, the weight loss and weight management market is segmented into meals, beverages, and supplements. In 2017, the beverages segment is expected to account for the largest share of the weight loss management market. By equipment, the weight loss management market is segmented into fitness equipment and surgical equipment. id=1152The weight loss management market is highly competitive, with the presence of several small and large players.

0

According to the new market research report "In Vitro Diagnostics Quality Control Market by Source (Plasma, Whole Blood, Urine), Technology (Immunoassay, Hematology, Microbiology, Molecular Diagnostics), Manufacturer (Third-party, OEM), End Users (Hospitals, Lab) - Global Forecast to 2026", published by MarketsandMarkets™, the global IVD Quality Control Market is projected to reach USD 1. Browse in-depth TOC on "In Vitro Diagnostics Quality Control Market"252 – Tables59 – Figures342 – PagesDownload PDF Brochure: https://www. Based on product & service, the IVD Quality Control Market is segmented into quality control products, data management solutions, and quality assurance services. Third-party controls accounted for the largest share for the IVD quality control marketBased on manufacturer, the In Vitro Diagnostics Quality Control Market is segmented into third-party controls and OEM controls. id=198032582Some of the key players in the In Vitro Diagnostics (IVD) Quality Control Market include Bio-Rad Laboratories, Inc.

0

According to the new market research report "Interventional Cardiology Market by type (Stents, Structural Heart, Catheters, Plaque Modification (Atherectomy), Hemodynamic Flow Alteration (Embolic Protection, Total Occlusion), Guidewire, Introducer Sheath, IVUS)) - Global Forecast to 2025", published by MarketsandMarkets™, the global Interventional Cardiology Devices Market size is projected to reach USD 21. Browse in-depth TOC on "Interventional Cardiology Devices Market"179 – Tables38 – Figures196 – PagesDownload PDF Brochure: https://www. Based on type, the angioplasty balloons market is segmented into old/normal balloons, cutting and scoring balloons, and drug-eluting balloons. id=548 North America accounted for the largest share of the interventional cardiology market in 2019. Some of the major players in the interventional cardiology devices market include Medtronic (US), Boston Scientific Corporation (US), Abbott (US), Cardinal Health (US), iVascular (Spain), Edward Lifescinces Corporation (US), B.

0

According to the new market research report "Genome Engineering Market by Technology (CRISPR, TALEN, ZFN, Antisense), Product & Service, Application (Cell Line Engineering, Genetic Engineering, Diagnostics, Drug Discovery & Development), End-User and Region - Global Forecast to 2025", published by MarketsandMarkets™, the global genome editing market is projected to reach USD 11. The CRISPR technology segment accounted for the largest share of the genome editing/genome engineering industry in 2019. Browse in-depth TOC on "Genome Engineering Market" 154 – Tables 28 – Figures 147 – Pages By end user, the pharmaceutical companies segment accounted for the largest share of the market. Pharmaceutical companies accounted for the largest share of the genome editing/genome editing market , by end user, in 2019. By application, the cell line engineering segment accounted for the largest share of the market Based on application, the genome editing/genome engineering market is segmented into cell line engineering, genetic engineering, diagnostic applications, drug discovery & development, and other applications.

0

The vital sign monitoring device segment accounted for the largest share of the Clinical-Grade Wearable market in 2019Based on device type, the vital sign monitoring segment accounted for the largest share of the Clinical Wearable Market in 2019. Browse in-depth TOC on "Medical Wearable Devices Market"120 – Tables30 – Figures171 – PagesThe Patches product segment accounted for the largest share of the Clinical-Grade Wearable market in 2019Based on product type, the patches segment accounted for the largest share of the Clinical Wearable Market in 2019. In 2019, the Long-term Care Centers/ Assisted Living Facilities/Nursing Homes accounted for the largest share and highest growth of the Clinical-Grade Wearable market. New communication technologies majorly drive growth in this market segment are supporting the transition of healthcare delivery from institution-centric frameworks to patient-centric care. id=52426876The prominent players in this medical wearable devices market are Medtronic plc.

0

According to the new market research report "Defibrillators Market by Product [Implantable Cardioverter Defibrillator (Transvenous ICD, Single & Dual Chamber, CRT-D, S-ICD), External (Manual, AED, Wearable)], End User (Hospitals, Pre-hospital, Public Access, Home care) - Global Forecast to 2025", published by MarketsandMarkets™, the Defibrillators Market is projected to reach USD 11. Browse in-depth TOC on "Defibrillators Market"132 – Tables30 – Figures158 – PagesThe ICDs segment accounted for the largest share of the market in 2019On the basis of type, the market is segmented into implantable cardioverter defibrillators (ICDs) and external defibrillators. The ICDs market is further segmented into transvenous implantable cardioverter defibrillators (T-ICDs) and subcutaneous implantable cardioverter defibrillators (S-ICDs). The External Defibrillators Market is further segmented into manual and semi-automated external defibrillators, fully automated external defibrillators, and wearable cardioverter defibrillators (WCDs). id=549Prominent players in the Defibrillators Market include Medtronic (Ireland), St.

0

id=197226392The growth of the global Hemostasis Analyzer Market is largely driven by the increasing prevalence of cardiovascular diseases and blood disorders, technological advancements in coagulation analyzers, and the rising geriatric population. Browse in-depth TOC on "Hemostasis Analyzer Market"105 – Tables24 – Figures155 – PagesOptical technology segment accounted for the largest share of the Coagulation Analyzer Market, by technology, in 2019The coagulation analyzers available in the market are based on three major technologies—optical technology, mechanical technology, and electrochemical technology. The most widely used technology in the Hemostasis Analyzer Market is the optical technology. North America is the largest regional market for coagulation analyzersNorth America (comprising the US and Canada) accounted for the largest share of the global Hemostasis Analyzer Market in 2019, followed by Europe. (US), Sysmex Corporation (Japan), Nihon Kohden Corporation (Japan), Diagnostica Stago (France), Helena Laboratories (US), and Horiba Medical (Japan) are some of the key players operating in this Hemostasis Analyzer Market.

0

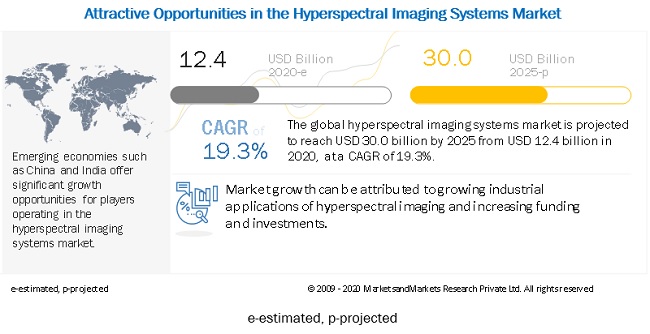

According to the new market research report "Hyperspectral Imaging Market by Product (Camera, Accessories), Technology (Snapshot, Push broom), Application (Military, Remote Sensing (Agriculture, Mining, Environmental), Machine Vision, Life Sciences & Medical Diagnosis) - Global Forecast to 2025", published by MarketsandMarkets™, the Hyperspectral Imaging System Market is projected to reach USD 30. In 2019, the cameras segment accounted for the largest share of the marketOn the basis of product, the Hyperspectral Imaging Market is segmented into cameras and accessories. Technological advancements, the development of affordable hyperspectral imaging cameras, and the increasing adoption of hyperspectral technology for defense and industrial applications are driving the growth of the hyperspectral cameras segment. This can be attributed to the advantages offered by snapshot hyperspectral imaging systems, which make this technology most suitable for real-time analysis. id=246979343The prominent players operating in the Hyperspectral Imaging Market include Headwall Photonics, Inc.

0

7% between 2020 and 2025Browse in-depth TOC on "AI in Genomics Market"141 – Tables24 – Figures154 – PagesDownload PDF Brochure: https://www. The machine learning segment dominated this market in 2019, as pharmaceutical companies, CROs, and biotechnology companies have widely adopted machine learning for drug genomics applications. This is because machine learning can extract insights from data sets, accelerating genomic research. North America is the largest regional market for AI in Genomics in 2019In 2019, North America accounted for the largest share of the AI in Genomics market, followed by Europe. id=36649899Prominent players in the AI in Genomics Market are IBM (US), Microsoft (US), NVIDIA Corporation (US), Deep Genomics (Canada), BenevolentAI (UK), Fabric Genomics Inc.

0

According to the new market research report Contract Manufacturing in Medical Device Market is estimated to reach USD 113. The key factors driving the growth of the Contract Manufacturing in Medical Device Market include the overall growth of the medical devices market, mainly due to rising disease prevalence, life expectancy, and the geriatric population. id=170622851However, market growth is impeded by the growing consolidation in the medical devices market. Class II medical devices segment accounted for the largest share of the Contract Manufacturing in Medical Device Market in 2020. In 2020, the device development and manufacturing services segment accounted for the largest share of the marketBased on service, the medical device contract manufacturing market is segmented into device development and manufacturing services, quality management services, packaging and assembly services and other services.

According to the new market research report "In Vitro Diagnostics Quality Control Market by Source (Plasma, Whole Blood, Urine), Technology (Immunoassay, Hematology, Microbiology, Molecular Diagnostics), Manufacturer (Third-party, OEM), End Users (Hospitals, Lab) - Global Forecast to 2026", published by MarketsandMarkets™, the global IVD Quality Control Market is projected to reach USD 1. Browse in-depth TOC on "In Vitro Diagnostics Quality Control Market"252 – Tables59 – Figures342 – PagesDownload PDF Brochure: https://www. Based on product & service, the IVD Quality Control Market is segmented into quality control products, data management solutions, and quality assurance services. Third-party controls accounted for the largest share for the IVD quality control marketBased on manufacturer, the In Vitro Diagnostics Quality Control Market is segmented into third-party controls and OEM controls. id=198032582Some of the key players in the In Vitro Diagnostics (IVD) Quality Control Market include Bio-Rad Laboratories, Inc.

Based on product, the market is segmented into thoracic fusion and lumbar fusion devices, cervical fusion devices, spine biologics, non-fusion devices, vertebral compression fracture treatment devices, spinal decompression devices, and spine bone stimulators. Browse in-depth TOC on "Spinal Implants Market"314 – Tables32 – Figures269 – PagesThe spinal fusion and fixation technologies segment accounted for the largest share of the Spinal Implants Devices Market in 2019. On the basis of technology, the Spinal Surgery Devices Market is segmented into spinal fusion and fixation, vertebral compression fracture treatment, motion preservation/non-fusion, and spinal decompression technologies. North America dominates the Spinal Implants Market. id=712The major players operating in the Spinal Implants Market are Medtronic (Ireland), DePuy Synthes (US), NuVasive, Inc.

According to the new market research report "Interventional Cardiology Market by type (Stents, Structural Heart, Catheters, Plaque Modification (Atherectomy), Hemodynamic Flow Alteration (Embolic Protection, Total Occlusion), Guidewire, Introducer Sheath, IVUS)) - Global Forecast to 2025", published by MarketsandMarkets™, the global Interventional Cardiology Devices Market size is projected to reach USD 21. Browse in-depth TOC on "Interventional Cardiology Devices Market"179 – Tables38 – Figures196 – PagesDownload PDF Brochure: https://www. Based on type, the angioplasty balloons market is segmented into old/normal balloons, cutting and scoring balloons, and drug-eluting balloons. id=548 North America accounted for the largest share of the interventional cardiology market in 2019. Some of the major players in the interventional cardiology devices market include Medtronic (US), Boston Scientific Corporation (US), Abbott (US), Cardinal Health (US), iVascular (Spain), Edward Lifescinces Corporation (US), B.

Browse and in-depth TOC on "Minimally Invasive Surgical Instruments Market"237 - Tables43 - Figures274- PagesDownload PDF Brochure: https://www. Emerging economies such as China, Japan, and India are providing lucrative opportunities for the players operating in the MIS Instruments Market. The handheld instruments segment accounted for the largest share of the minimally invasive surgical instruments market, by product segment, in 2020Based on product, the market is segmented into handheld instruments, inflation devices, surgical scopes, cutting instruments, guiding devices, electrosurgical & electrocautery instruments, and other instruments. In 2020, the hospitals and specialty clinics segment accounted for the largest share of the minimally invasive surgical instruments market. North America is the largest regional market for minimally invasive surgical instruments marketThe global MIS Instruments Market is segmented into five major regions—north America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa.

According to the new market research report "Genome Engineering Market by Technology (CRISPR, TALEN, ZFN, Antisense), Product & Service, Application (Cell Line Engineering, Genetic Engineering, Diagnostics, Drug Discovery & Development), End-User and Region - Global Forecast to 2025", published by MarketsandMarkets™, the global genome editing market is projected to reach USD 11. The CRISPR technology segment accounted for the largest share of the genome editing/genome engineering industry in 2019. Browse in-depth TOC on "Genome Engineering Market" 154 – Tables 28 – Figures 147 – Pages By end user, the pharmaceutical companies segment accounted for the largest share of the market. Pharmaceutical companies accounted for the largest share of the genome editing/genome editing market , by end user, in 2019. By application, the cell line engineering segment accounted for the largest share of the market Based on application, the genome editing/genome engineering market is segmented into cell line engineering, genetic engineering, diagnostic applications, drug discovery & development, and other applications.

Browse in-depth TOC on "AEDs Market"132 – Tables30 – Figures158 – PagesThe ICDs segment accounted for the largest share of the market in 2019On the basis of type, the market is segmented into implantable cardioverter defibrillators (ICDs) and external defibrillators. The ICDs market is further segmented into transvenous implantable cardioverter defibrillators (T-ICDs) and subcutaneous implantable cardioverter defibrillators (S-ICDs). The External Defibrillators Market is further segmented into manual and semi-automated external defibrillators, fully automated external defibrillators, and wearable cardioverter defibrillators (WCDs). The ICDs segment accounted for the largest share of the market in 2019. In 2019, North America accounted for the largest share of the Defibrillators MarketIn 2019, North America accounted for the largest share of the market.

The vital sign monitoring device segment accounted for the largest share of the Clinical-Grade Wearable market in 2019Based on device type, the vital sign monitoring segment accounted for the largest share of the Clinical Wearable Market in 2019. Browse in-depth TOC on "Medical Wearable Devices Market"120 – Tables30 – Figures171 – PagesThe Patches product segment accounted for the largest share of the Clinical-Grade Wearable market in 2019Based on product type, the patches segment accounted for the largest share of the Clinical Wearable Market in 2019. In 2019, the Long-term Care Centers/ Assisted Living Facilities/Nursing Homes accounted for the largest share and highest growth of the Clinical-Grade Wearable market. New communication technologies majorly drive growth in this market segment are supporting the transition of healthcare delivery from institution-centric frameworks to patient-centric care. id=52426876The prominent players in this medical wearable devices market are Medtronic plc.

According to the new market research report The laboratory information systems market is projected to reach USD 2. id=232312738By delivery mode, cloud-based LIS to register the highest CAGR during the forecast periodBased on delivery mode, the LIS market is segmented into on-premise and cloud-based LIS. The cloud-based LIS segment is expected to register the highest CAGR during the forecast period. By product, the standalone LIS segment accounted for the largest market share in 2018Based on product, the LIS market is segmented into standalone LIS and integrated LIS. North America dominated the LIS market in 2018; this trend to continue during the forecast periodGeographically, the LIS market is divided into North America, Europe, Asia Pacific, and the Rest of the World (RoW).

According to the new market research report "Defibrillators Market by Product [Implantable Cardioverter Defibrillator (Transvenous ICD, Single & Dual Chamber, CRT-D, S-ICD), External (Manual, AED, Wearable)], End User (Hospitals, Pre-hospital, Public Access, Home care) - Global Forecast to 2025", published by MarketsandMarkets™, the Defibrillators Market is projected to reach USD 11. Browse in-depth TOC on "Defibrillators Market"132 – Tables30 – Figures158 – PagesThe ICDs segment accounted for the largest share of the market in 2019On the basis of type, the market is segmented into implantable cardioverter defibrillators (ICDs) and external defibrillators. The ICDs market is further segmented into transvenous implantable cardioverter defibrillators (T-ICDs) and subcutaneous implantable cardioverter defibrillators (S-ICDs). The External Defibrillators Market is further segmented into manual and semi-automated external defibrillators, fully automated external defibrillators, and wearable cardioverter defibrillators (WCDs). id=549Prominent players in the Defibrillators Market include Medtronic (Ireland), St.

According to the new market research report "Medical Radiation Detection, Monitoring and Safety Market by Detector (Gas-Filled, Scintillators, Solid-State), Product (Personal Dosimeters, Passive Dosimeters) Safety (Full-Body Protection) & End User (Hospitals, Non-Hospitals) - Global Forecast to 2027", published by MarketsandMarkets™, the global Medical Radiation Detection, Monitoring, and Safety Market is projected to reach USD 1. Browse in-depth TOC on "Medical Radiation Detection, Monitoring, and Safety Market"401 – Tables42 – Figures336 – PagesDownload PDF Brochure: https://www. Emerging economies such as China, Japan, and India are providing lucrative opportunities for the players operating in the medical radiation detection & safety market. id=1200 Full-body protection segment accounted for the largest share in the market, by medical radiation safety productsThe medical radiation detection, monitoring, & safety market is segmented into full-body protection products, face protection products, hand safety products, and other medical radiation safety products. North America is the largest regional market for medical radiation detection, monitoring, & safety marketThe global medical radiation detection market has been segmented into four major regions—North America, Europe, the Asia Pacific, and Rest of the World.

id=197226392The growth of the global Hemostasis Analyzer Market is largely driven by the increasing prevalence of cardiovascular diseases and blood disorders, technological advancements in coagulation analyzers, and the rising geriatric population. Browse in-depth TOC on "Hemostasis Analyzer Market"105 – Tables24 – Figures155 – PagesOptical technology segment accounted for the largest share of the Coagulation Analyzer Market, by technology, in 2019The coagulation analyzers available in the market are based on three major technologies—optical technology, mechanical technology, and electrochemical technology. The most widely used technology in the Hemostasis Analyzer Market is the optical technology. North America is the largest regional market for coagulation analyzersNorth America (comprising the US and Canada) accounted for the largest share of the global Hemostasis Analyzer Market in 2019, followed by Europe. (US), Sysmex Corporation (Japan), Nihon Kohden Corporation (Japan), Diagnostica Stago (France), Helena Laboratories (US), and Horiba Medical (Japan) are some of the key players operating in this Hemostasis Analyzer Market.

This report aims to provide insights into the global cancer immunotherapy market. Browse 43 market data Tables and 69 Figures spread through 145 Pages and in-depth TOC on "Cancer Immunotherapy Market"Download PDF Brochure: https://www. id=197577894In this report, the global Cancer Immunotherapy Market has been segmented based on type, application, end user, and region. On the basis of end users, the global Cancer Immunotherapy Market is segmented into hospitals and clinics & others. On the basis of applications, the global Cancer Immunotherapy Market is segmented into lung cancer, breast cancer, colorectal cancer, melanoma, prostate cancer, head & neck cancer, and others.

According to the new market research report "Hyperspectral Imaging Market by Product (Camera, Accessories), Technology (Snapshot, Push broom), Application (Military, Remote Sensing (Agriculture, Mining, Environmental), Machine Vision, Life Sciences & Medical Diagnosis) - Global Forecast to 2025", published by MarketsandMarkets™, the Hyperspectral Imaging System Market is projected to reach USD 30. In 2019, the cameras segment accounted for the largest share of the marketOn the basis of product, the Hyperspectral Imaging Market is segmented into cameras and accessories. Technological advancements, the development of affordable hyperspectral imaging cameras, and the increasing adoption of hyperspectral technology for defense and industrial applications are driving the growth of the hyperspectral cameras segment. This can be attributed to the advantages offered by snapshot hyperspectral imaging systems, which make this technology most suitable for real-time analysis. id=246979343The prominent players operating in the Hyperspectral Imaging Market include Headwall Photonics, Inc.

Browse 143 Market Data Tables and 33 Figures spread through 187 Pages and in-depth TOC on "Weight Loss Obesity Management Market"Download PDF Brochure: http://www. id=1152Beverages segment to dominate the market in 2017Based on diet, the weight loss and weight management market is segmented into meals, beverages, and supplements. In 2017, the beverages segment is expected to account for the largest share of the weight loss management market. By equipment, the weight loss management market is segmented into fitness equipment and surgical equipment. id=1152The weight loss management market is highly competitive, with the presence of several small and large players.

7% between 2020 and 2025Browse in-depth TOC on "AI in Genomics Market"141 – Tables24 – Figures154 – PagesDownload PDF Brochure: https://www. The machine learning segment dominated this market in 2019, as pharmaceutical companies, CROs, and biotechnology companies have widely adopted machine learning for drug genomics applications. This is because machine learning can extract insights from data sets, accelerating genomic research. North America is the largest regional market for AI in Genomics in 2019In 2019, North America accounted for the largest share of the AI in Genomics market, followed by Europe. id=36649899Prominent players in the AI in Genomics Market are IBM (US), Microsoft (US), NVIDIA Corporation (US), Deep Genomics (Canada), BenevolentAI (UK), Fabric Genomics Inc.